How Credit Scores Effect Mortgage Interest Rates

The most influential factor in achieving better mortgage terms is your credit score. The higher your credit score is, the lower your monthly interest rates will be on your mortgage.

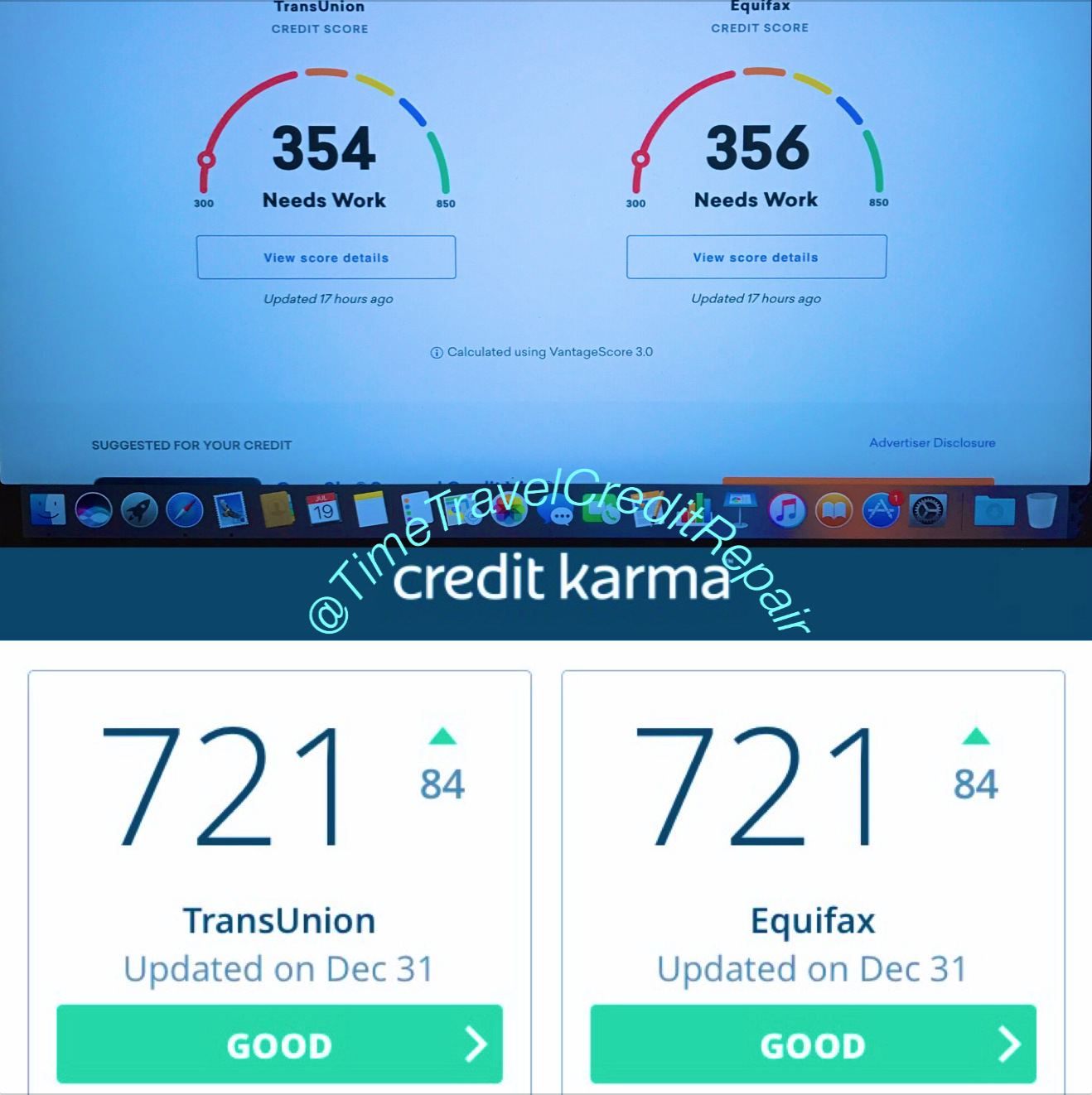

How your credit score will effect mortgage interest rates

In most circumstances a borrower that maintains a higher credit score will be approved for a lower interest mortgage rate. Below are a few credit score factors to consider:

- check

- check

- check

Aside from achieving a lower mortgage rate, your credit score is also a major influence in getting approved in the first place. A home buyer that has a FICO credit score of 620 or below is highly unlikely to even be approved. Bottom line, the more your able to boost your credit score and diversify your credit portfolio the better your odds will be in getting approved for a home purchase loan, as well as securing a lower monthly interest rate.

A consumer credit score of 740 or above will generally qualify for the best mortgage rates, depending on your lender. Considering lenders across the board, mortgage rates offered to the the highest and lowest credit tiers may vary as much a 1% to 1.5%.

See The Difference

Monthly principal and interest payments on a 30-year fixed-rate mortgage for $200,000

| Interest Rate | Monthly principal and interest |

| 4% | $954.83 |

| 5% | $1073.64 |

At the end of your mortgage term, your credit score can provide thousands of dollars in savings. Check your credit score today for only $1 at Privacy Guard, our go-to source for the most up to date credit report information.

Give Lenders What Their Looking For

There are four primary credit factors that lenders will look at when determining your eligibility for a home loan approval.

- check

- check

- check

- check

- check

- check

How to prepare your credit for a home purchase

One would be wise to begin their credit preparation process for a home purchase one full year in advance. Doing so will provide you ample time to correct all errors on your report which, in turn, will boost your score across all three bureaus.

Often times an individual will benefit greatly by utilizing a credit repair companies services for this process. With a working knowledge of how credit bureaus operate and consumer rights, credit repair services will thoroughly address everything that may hold you back from getting approved or achieving a lower interest rate.

What credit repair services can do

A reputable Credit repair service company can help expedite the process of restoring your credit report to a condition that will work for your individual goals.

Agencies will perform an initial consultation and request to either provide hard copies of your reports or suggest an affordable credit report provider that will generate your latest and most up today report. Once that is done a quality credit repair service will help you in addressing and disputing all negative marks that are eligible to be removed, or correct any miss representations of your personal information. In addition to this, they should consult with you on how to effectively build and diversify your credit portfolio through the application of qualifying primary credit lines. With open lines of communication, a credit repair company can be an invaluable asset when preparing for home ownership.